What's the biggest barrier to purchasing a home that requires a mortgage? For millions of college graduates — both older and younger millennials — it isn’t their credit card debt. Rather, it’s their student loans that are preventing them from fulfilling their dream of homeownership.

To explain it further, here’s the summary of the latest student loan debt statistics:

Statistics from personal finance site Make Lemonade reported that over 44 million people carry a collective debt of $1.5 trillion.

According to Student Loan Debt and Housing Report 2017: When Debt Holds You Back by the National Association of Realtors (NAR), 17% of borrowers owe more than $100,000 in student loans.

More than 7 in 10 student loan borrowers believe their debt has impacted their ability to purchase a home.

Student loan debt has now become the second highest consumer debt category - second only to mortgages.

Moreover, paying off their student loans isn’t the only challenge they encounter when qualifying for a mortgage.

Nonetheless, if you're a student loan borrower, there are steps you can take to overcome these hurdles. Homeownership doesn’t happen overnight, but anyone can make it happen with ample planning and preparation.

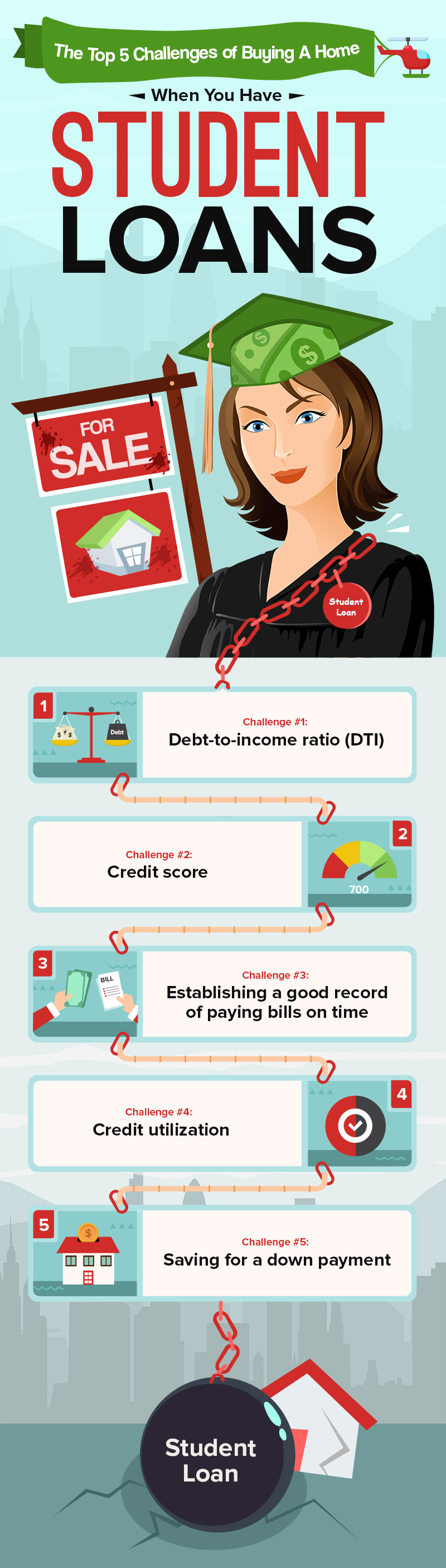

According to the NAR report, 52% of younger millennials don’t qualify for mortgages due to their debt-to-income ratios, which includes student loan debt. It’s one of the main things that delays a home purchase.

Your DTI ratio is simply what you owe compared to how much you make or the amount of recurring debt you have versus your monthly income. Most of the time, lenders focus on this ratio, more than your credit score, or even how much you have set aside for a down payment. They assess whether you can still balance your living expenses while paying off your debt obligations. As a rule of thumb, they want to see a low DTI, with a ratio, ideally, falling below 36%.

Your lender will also calculate both your front-end and back-end DTI to determine if you qualify for a mortgage loan. The front-end DTI is known as the housing ratio, which is the amount of monthly gross income spent on housing expenses. On the other hand, the back-end ratio includes all of your debt obligations, such as student debt, car payments, and credit card bills.

Pro tip: Control and reduce your DTI.

Before house-hunting, try to reduce your DTI by paying existing debt and/or increasing your income. If you have credit card debt, remember that most lenders will use the minimum payment balance when calculating your ratio. With that said, it's ideal to pay off your debt every month to reduce the amount of money paid in interest.

While a high percentage of student loan borrowers are denied mortgages because of steep DTI ratios, your credit score plays a role as well. Your ranking affects whether you get a low mortgage interest rate, although only 8% of millennials were denied because of a low credit score.

The average FICO credit score is 700. A credit score of 750 or higher is considered excellent while a score of 649 below is considered poor.

Pro tip: Build up your credit score—the higher, the better!

If you're hoping to get a mortgage, paying your debts on time will help boost your credit score. Keep your score healthy by not skipping or missing any of your payments. Check your credit report every year and if you find any errors, take the necessary steps to resolve them.

The most important factor in your credit score is your payment history. It must show that you are not only financially capable but also responsible when making payments. Lenders prefer to lend their money to a borrower who has a solid financial reputation.

Pro tip: Avoid skipping any payments and always pay on time.

To avoid being late, you can set up auto-pay for all your accounts to ensure you'll make full and on-time payments. If you have a delinquent payment, pay the balance so you don’t damage your credit score and can start to build a good payment history.

Aside from your credit score and DTI, lenders will also evaluate your credit card utilization. It is your monthly credit card spending as a percentage of your credit limit, which should be less than 30%.

Pro tip: Keep it low.

The ideal way to manage your credit utilization is by using as little of your available credit as possible. For example, if you have a $3,000 credit limit and you spent $1,000 in one month, your credit utilization is 30%. It's even better if you can keep your utilization at less than 10%. You can set up automatic balance alerts to monitor your credit utilization and pay off your balance multiple times a month to reduce it.

Whether you're a student loan borrower or not, it’s understandable that the biggest challenge of purchasing a home is saving for a down payment. At least 85% of non-homeowners say their inability to save for a down payment has delayed their ability to buy a home.

Pro tip: Look for down payment assistance and other ways of saving.

Look out for government assistance programs available to first-time buyers and student loan borrowers. Federal programs, such as the FHA or USDA loans, will allow you to purchase a home with less than 3.5% down. Likewise, there are existing local programs where you might qualify. Don't be afraid to check out their eligibility requirements or talk to a mortgage lender to help you understand the process.

Another thing you can do is to look for creative ways to save for a down payment. Even if that means delaying your dream of homeownership for a few years, try saving all “found” money that comes down your way. To achieve this, you can save any money you got from bonuses, overtime pay, and cash gifts from relatives and friends or even allocate income tax refunds to be used specifically for your down payment and closing costs when it comes time for you to buy a home.

To get a lower monthly payment so you can manage your finances better, see if you can refinance or consolidate your student loans. However, it still depends on your circumstances and if you're confident in handling your monthly payments. Before you start house-hunting, just remember to set a realistic budget and focus on your financial goals to finally achieve the American Dream.

Coming Soon

Downtown Woodstock, GA

7680 Main Street

Woodstock, GA