What is an appraisal?

An appraisal is a professional estimate of the value of a home done by a certified appraiser. It is a critical process for buyers because lenders always require a home appraisal before they issue a mortgage. Meanwhile, for sellers, a good understanding of the appraisal process will help them understand how their home's value is determined.

Here, we uncover the most common home appraisal myths to help both sellers and buyers better understand this valuable process in real estate.

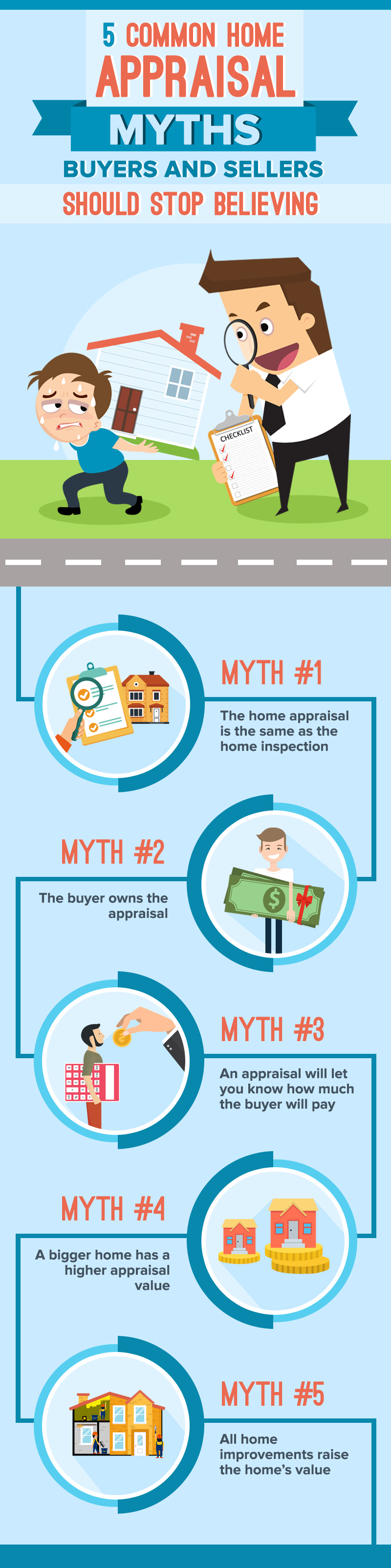

Myth #1: The home appraisal is the same as the home inspection

This is probably the most common home appraisal myth that most buyers and sellers believe. While the home inspection and home appraisal are both used to determine the condition of a property to protect the buyer and the buyer's lender, the two tasks are entirely different. A home inspection is done to identify issues with a home. The home inspector looks for issues that all parties should be aware of before the deal goes on. It is the inspector’s job to look for anything that might be problematic, like mold manifestations, problems with the foundation, plumbing and electrical problems, roof issues, and so on.

The appraiser’s job, on the other hand, is to find the objective market value of the property. The appraiser will look into similar homes in the area that have been sold recently, also known as “comps,” to determine a value. Yes, it’s the same thing you and your realtor used to come up with a list price. Appraisers also take into account your home’s condition, square footage, location, and quality and use the information to make their accurate assessment of how much your home is worth.

The only time an appraiser also takes the role of a home inspector is when the borrower is getting an FHA or a VA loan. In that case, the appraiser will also look for certain deficiencies in a home and may flag those problems during an appraisal.

Myth #2: The buyer owns the appraisal

Since the buyer pays the appraisal, does the appraisal belong to the buyer?

It’s easy to assume that the appraiser works for the buyer. However, while the buyer certainly pays for the appraisal, the appraiser actually works for the lender. An article written by Ryan Lundquist, a certified appraiser, shows a copy of an appraisal report and clears up this common misconception. An appraisal report during a typical loan indicates that the client listed is the lender and that the buyer is listed as the user.

It is the lender who engages the appraiser to do the job. The appraisal is actually an “investigation” to protect the buyer’s lender from a bad deal. The report will help the lender evaluate the property and make a decision about the loan. Rest assured, appraisers are trained to be unbiased and ethical. It’s also a crime to put any pressure on appraisers for them to come up with a certain value. Likewise, a buyer is also legally entitled to have a copy of the appraisal from the lender, especially in Fannie Mae or Freddie Mac mortgages.

Myth #3: An appraisal will let you know how much the buyer will pay

Rather than being an exact science, the appraisal is only an opinion of a home’s value based on the comps and the actual condition of the home. It could never indicate how much the buyer should pay, or how much the seller should accept to complete the deal. The appraisal report only provides guidance to the lender and serves as a safeguard for his/her investment.

If the appraisal doesn’t match the contract price or if the home is appraised lower than the price the seller and buyer agreed upon, discussions will proceed on who pays for the shortfall. No, the lender definitely isn’t going to give more money to cover the difference. Instead, the seller and buyer can agree to negotiate a new purchase price that will match the appraisal.

Myth #4: A bigger home has a higher appraisal value

The biggest home in the area doesn’t guarantee that it will be appraised way higher than its neighboring homes. In fact, having an exceptional home in an otherwise average neighborhood can actually do more harm than good. An appraiser will greatly consider the size and amenities of other homes in your neighborhood to determine the price of your home. If your home is super-sized but is actually surrounded by lower-priced homes, its value will still be lowered. The real estate cliche that says it’s better to “buy the worst house in the best block” is still true. It’s because being surrounded by higher-priced homes will also bring up your home’s value, so location remains a top factor.

Myth #5: All home improvements raise the home’s value

It isn’t surprising that most sellers assume they will get equal value for every home improvement project they complete. But what they don’t know is that there are some home improvements that could actually lower its value, and appraisers won’t actually applaud you for those. If you converted your garage into another living space or removed a bedroom to give way to a bigger room, well, you may be in for a surprise. Appraisers base their judgment on measurable aspects of the house, such as the square footage, number of rooms, the home’s foundation, and others. So it’s important to note that every necessary home feature should serve its primary purpose. Having four bedrooms in a neighborhood with mostly three-bedroom houses can bring up your home’s value more than a fancy garage-to-gym conversion.

Likewise, overly improving your house with intricate amenities that don’t even exist in surrounding homes won’t be beneficial. It’s because there will be no nearby sales data that the appraiser can use to evaluate how much those amenities are worth. When it comes to home appraisals, not all renovations can proportionally raise your home’s value, so be careful and educate yourself before removing or adding any amenities.

Bottom Line

Thankfully, working with a trusted local real estate agent can help a seller be more prepared for the home appraisal. Realtors can fill in any information that can be beneficial to the process since they understand what appraisers are looking for. They can look up comparable properties and they know and understand the local market where the home is located. Realtors can also help a seller point out the features and improvements on the property that can help increase its worth.

Woodstock, GA

7680 Main St

Suite 100

Woodstock, GA 30188

Stockbridge, GA

105 N Park Trl

Suite 200

Stockbridge, GA 30281

Duluth - Coming Soon

700 Satellite Place

Suite 125

Duluth, GA 30096